2024 was a momentous year for many reasons

England nearly brought it home in the Euros and many athletes did strike gold in the Paris Olympics and paralympics.

Millions of voters went to the polls in the UK and US, Darts sensation Luke Littler burst onto the scene as former US President and statesman Jimmy Carter departed after a century of public service.

It was also the year that we all felt better about our own parties and celebrations after seeing the disastrous Willy Wonka experience unfold in Glasgow!

For many other businesses 2024 was also a trial by fire with many continuing to struggle against stubborn debts, rising costs and wavering customer confidence.

But what does the data tell us about what happened in the previous 12 months for businesses?

The Insolvency Service have released their latest corporate insolvency figures for December 2024 which allows us to look at the previous year as a whole and look at all the major trends and undercurrents across the whole country and nations about what happened to business through the eye of insolvency procedures.

2024 Analysis

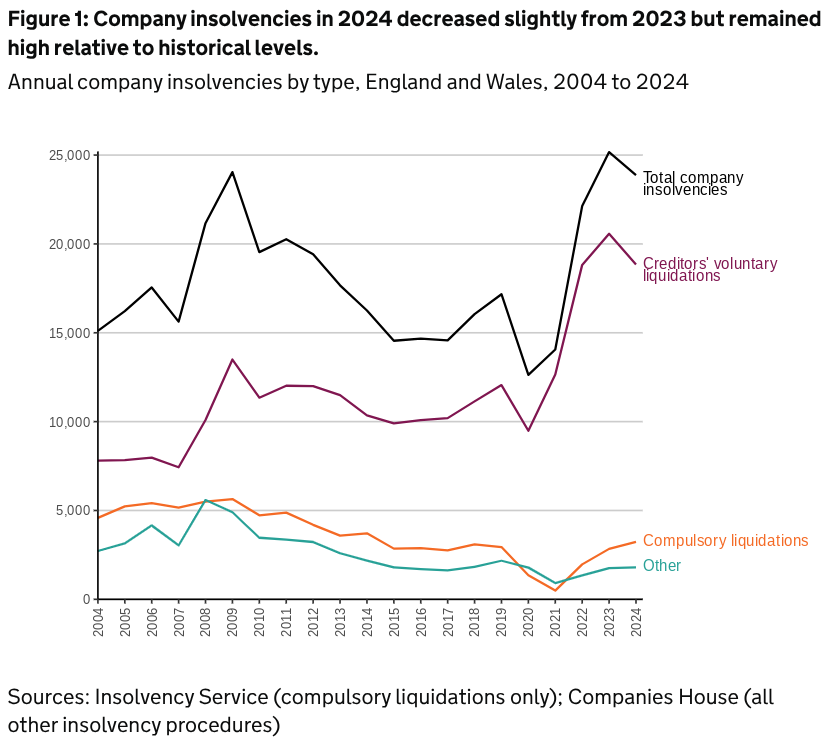

There were a total of 23,872 registered company insolvencies in 2024.

This was a 5% reduction on the 2023 total which was the highest number of procedures recorded since 1993.

| Year | Compulsory Liquidations | CVLs | Administrations | CVAs | Receiverships | Total |

| 2020 | 1,353 | 9,488 | 1,527 | 260 | 3 | 12,631 |

| 2021 | 491 | 12,655 | 796 | 115 | 1 | 14,058 |

| 2022 | 1,965 | 18,821 | 1,231 | 111 | 1 | 22,129 |

| 2023 | 2,838 | 20,570 | 1,567 | 186 | 2 | 25,163 |

| 2024 | 3,230 | 18,840 | 1,597 | 202 | 3 | 23,872 |

| Total | 9,877 | 80,374 | 6,718 | 874 | 10 | 97,853 |

Even though they were 8% lower than the previous year, total company insolvency numbers were again driven by creditor voluntary liquidations (CVLs) which were the most procedure seen making up 79% of all cases.

This was followed by compulsory liquidations (14%); administrations (7%) and company voluntary arrangements (CVAs) (less than 1%). There were also three receivership appointments in 2024, one more than in 2023.

While compulsory liquidations accounted for a greater proportion of insolvencies in 2024 compared to the year before, the proportion was actually lower than five years ago due to an increase in the number of CVLs over this period.

In 2019, CVLs made up only 70% of all cases whereas compulsory liquidations made up 17%, administrations 11% and CVAs 2% respectively.

The number of company insolvencies peaked during the 2008/09 recession following the gradual decline seen over the early 2000s. Volumes rose during 2018 and 2019 before falling to the lowest monthly volumes on record during the Covid-19 pandemic in 2020 and 2021, when additional government support measures were in place.

CVL numbers then increased in 2022, exceeding pre-pandemic levels while compulsory liquidations and administration numbers remained low.

Insolvency numbers increased further in 2023 to a 30-year-high with CVLs at a record high and compulsory liquidations at levels similar to 2015 to 2019.

In 2024, CVLs decreased by 8% from the record-high volumes registered in 2023.

Between 2017 and 2019, CVLs had been rising at approximately 10% per year but during the Covid-19 pandemic years they fell to their lowest levels since 2007. The number then increased between 2021 and 2023.

Compulsory Liquidations

Last year compulsory liquidations were at their highest levels since 2014 having increased by 14% compared to 2023 volumes.

This continued an increase from record low levels seen in 2020 and 2021 while restrictions applied to the use of statutory demands and certain winding-up petitions that led to compulsory liquidations.

Administrations

The number of administrations increased by 2% annually in 2024 and was also slightly higher than the annual totals seen between 2015 and 2019.

Administrations have continued to increase since 2022 from an 18-year annual low seen during the Covid pandemic in 2021.

CVAs

In 2024, the number of CVAs was 9% higher than in 2023 and over 80% higher than in 2022, which saw the lowest ever annual total in the time series going back to 1993.

Despite this increase, the number in 2024 was slightly less than 60% of the 2015 to 2019 annual average.

Rolling insolvency average

One in 191 companies on the Companies House effective register entered insolvency in 2024 which was a rate of 52.4 per 10,000 companies.

This is a decrease from the rate of 57.2 per 10,000 recorded in 2023.

The 2024 insolvency rate is much lower than the peak of 111.1 per 10,000 companies that was seen during the 2008/09 recession even though 2023 and 2024 saw similar numbers of insolvencies to 2008 and 2009. This is because the number of companies on the effective register has more than doubled.

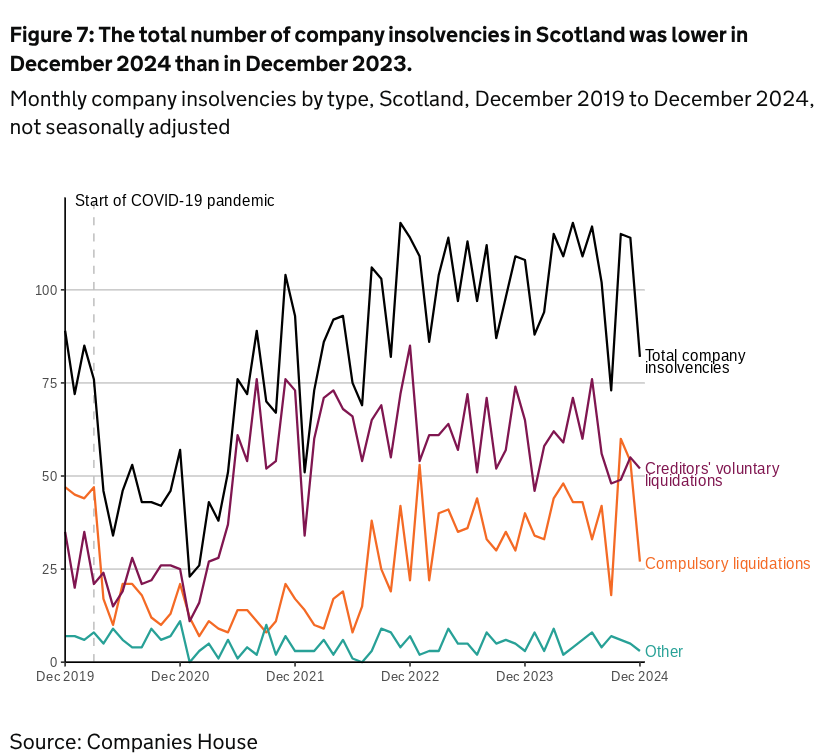

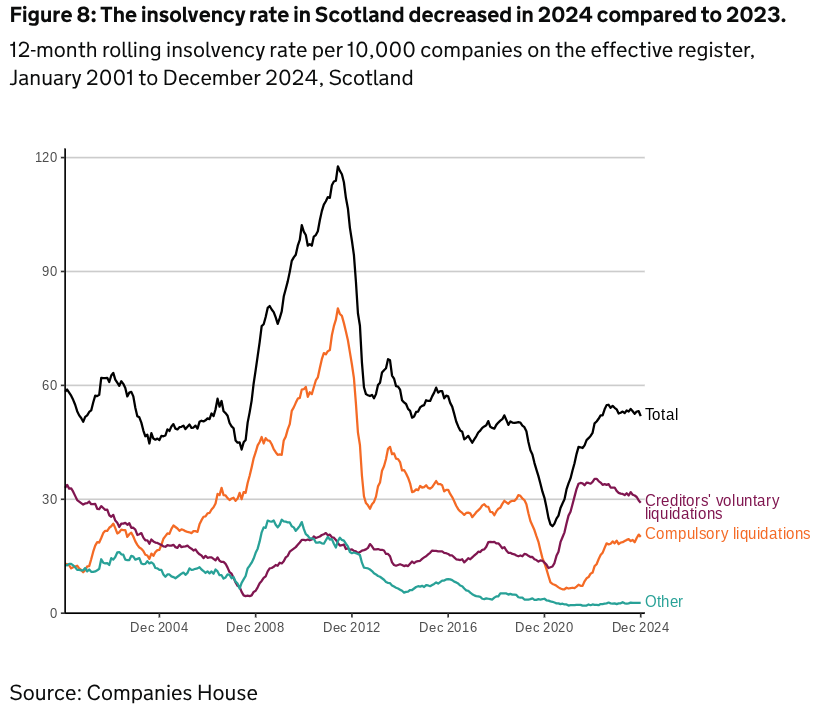

Scotland

There were 1,236 corporate insolvencies in Scotland in 2024 which is slightly higher than the total of 1,234 for 2023.

Historically, compulsory liquidations are the most common type of company insolvency in Scotland however, since 2020, numbers of CVLs have been higher.

The total insolvency rate in Scotland in 2024 was 51.9 per 10,000 on the Companies House effective register – this is down by 1.8 from the 53.7 per 10,000 recorded in 2023.

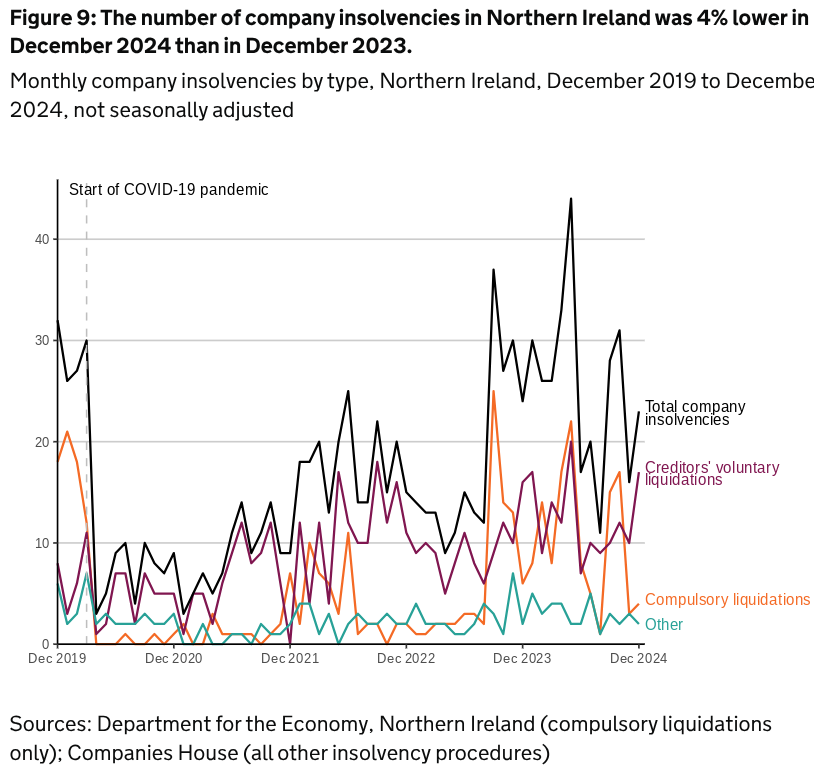

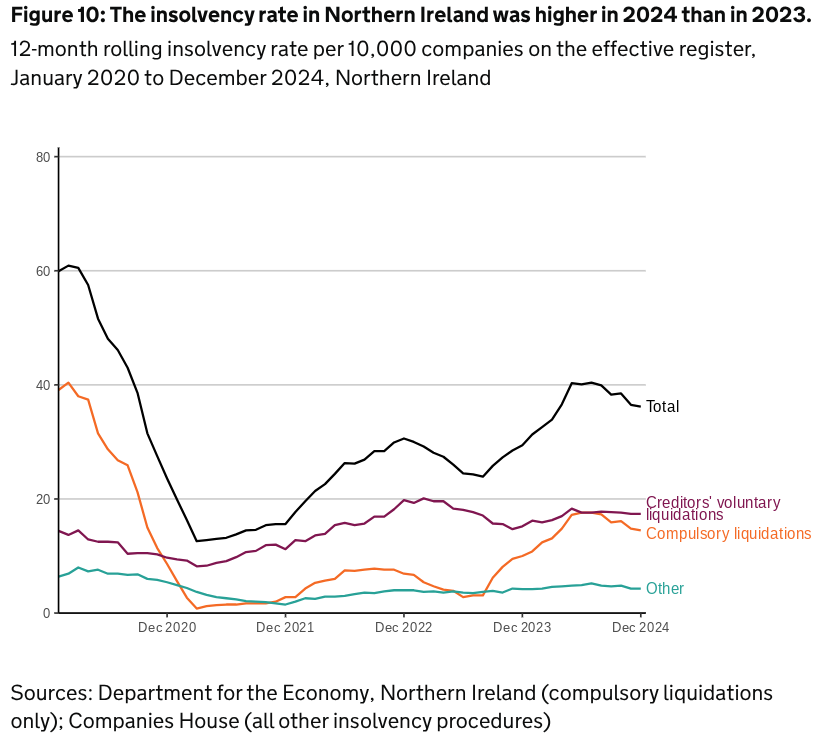

Northern Ireland

The annual number of insolvencies in Northern Ireland in 2024 was 305, which was a 40% increase from the 218 recorded in 2013.

Northern Ireland’s total insolvency rate in 2024 was 36.2 per 10,000 companies on the effective register which is an increase of 6.8 from the 29.4 recorded in December 2023.

Tim Cooper, President of R3, the UK’s insolvency and restructuring trade body said: “Despite a year-on-year decline in corporate insolvency numbers, the figures for this year are still higher than in 2022 and well above pre-pandemic levels.

“Compulsory liquidation levels have increased compared to last year as creditors pursue the debts they are owed in an effort to balance their own books.

Creditors’ voluntary liquidation (CVL) numbers have declined compared to 2023 while they too are higher than in 2022 and the years before and during the pandemic as a high volume of directors close their businesses now while the decision to do so still rests in their hands.

“2024’s insolvencies have been driven by another year of high costs and a series of political, economic and geopolitical events which have taken a toll on businesses especially in England and Wales.

“Members have told us that the Election, the Budget and the conflict in the Middle East have all led to increases in enquiries and requests for advice and support, and this reflects how these unexpected shocks can be and have been the tipping point for many businesses after years of battling harsh trading conditions.

“From a sectoral perspective retail, hospitality and construction have all suffered this year. All three of these industries have been hit hard by continued rises in expenses, while retail and hospitality have been affected by cautious consumer spending over the past 12 months and construction by bad weather and the delay to project starts and commissions caused by the General Election.

“These sectors are going to be some of the most affected by the Chancellor’s planned increases in Minimum Wage, Living Wage and Employers’ National Insurance Contributions. Although it’s likely we won’t see the impact of these on corporate insolvency figures until the end of the first or possibly the middle of the second quarter of next year, the prospect of their introduction is already causing concern for businesses right across the economy.

“Restructuring plans have been a major and consistent topic of conversation in the profession this year. The Tasty plc ruling in May opened up this process to mid-market firms and since it was made we’ve seen a number of recognisable names enter one in an attempt to resolve their financial issues.

“The challenge the profession faces is making restructuring plans accessible to the SME market – and given the positive impact this could have on local communities and supply chains by keeping viable SMEs open, I hope it can be achieved this year.”

You don’t have to wait until next month for January’s insolvency statistics to be released if your business is facing some familiar financial challenges.

You can get in touch with us right now to arrange a free initial consultation to discuss what options you have available depending on your unique circumstances.

No matter what your aims and objectives are for 2025, these will become clearer after talking with one of our advisors – or even give you new options you hadn’t thought or didn’t realise were available.